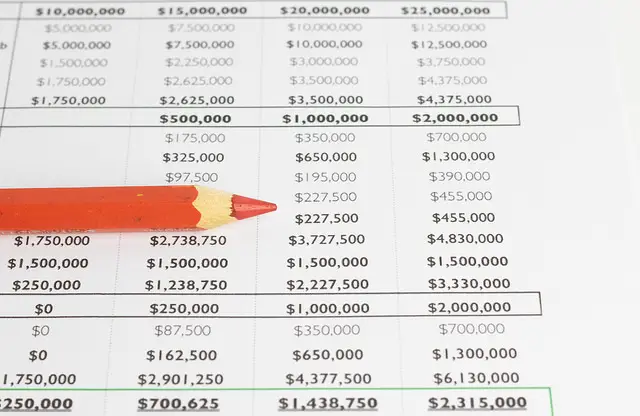

I’ve been faithfully watching my personal finances and tracking household costs for almost 20 years, Bill. (spreadsheet for tracking expenses)

You ask: How diligent?

I can tell you that in February 1998, my cable bill was $7.04, and in 2006, I paid $142.15 for an annual subscription to the Los Angeles Times.

I can also confirm that 6.5% of my income in 2007 went toward food, and that I spent $87.94 at my local K-Mart in August 2001. Just don’t ask me why, because I’m not that diligent with my record keeping.

How to invest in your 20s: 5 tips to get started

Why Tracking Expenses Is Important

Taking the effort to track and evaluate your money and where it goes is an important part of managing your personal finances. That’s because doing so reveals hidden money leaks, allowing you to better utilize your resources and ensure you always get the most out of your income.

It also makes it easy to set financial goals. Of course, before you can track your spending, you need to record them.

While not impossible, keeping track of all your cash purchases can be tedious and time-consuming. On the other hand, everything you buy with your credit or debit card is automatically recorded and available for review online or as part of your monthly billing statement – which is why I use credit cards as much as possible.

There are numerous alternatives for tracking your spending habits.

Now, I understand that many people are drawn to sites like Mint, OneBudget, Empower, and MyBudget-Online because their automation capabilities make managing your money practically painless.

Advantage of Spreadsheets

For me, the more traditional hands-on method is the only way to go; I use my own custom-designed Excel spreadsheet since it requires me to actively handle my personal funds. It also affords me more control than using a web-based service such as Mint.

True, a spreadsheet isn’t as appealing as automatic money-tracking web-based tools, but it’s the tried-and-true approach I’ve been using to manage my income, net worth, and expenses for over 20 years.

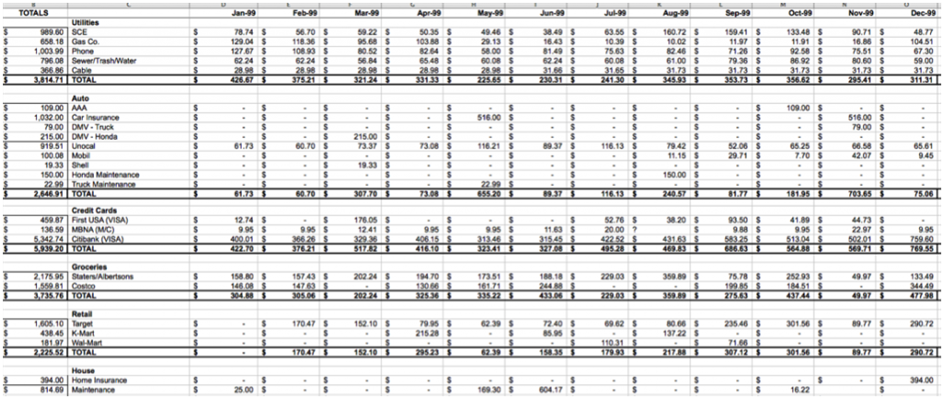

Here’s a small piece of the Excel worksheet for my household costs in 1999:

Although the custom Excel spreadsheet I created was initially modest, it has increased in detail and complexity over time, including pie charts and graphs that clearly depict the consequences of our household expenditure and present trending patterns.

Today, my spreadsheet categorizes our home spending into 13 broad categories and 50 subcategories. The primary categories are:

· Loans

· Utilities

· Medical & Dental

· Automobile Expenses

· Groceries

· House Expenses (excluding the mortgage)

· Entertainment

· Taxes

· ATM Withdrawals

And A Few More Quick Tips …

- If you are just getting started, make sure to set up an hour once a month to analyze your checkbook, receipts, and credit card statements, as well as record your expenses in a spreadsheet.

- Regularly updating your financial spreadsheet prevents errors on billing bills and keeps you on track with record keeping.

- If you’re not an Excel specialist, don’t worry; Microsoft has a plethora of budgeting worksheet templates that you can download and customize to meet your specific needs. In fact, the personal budget spreadsheet template has been downloaded more than 3.6 million times.

- Don’t be afraid if you’ve never used a spreadsheet before; they’re easy to use! Yes, spreadsheets are tremendously powerful tools when used properly. Most people, however, can master the fundamentals of accurately tracking their costs in less than 30 minutes.

- OpenOffice offers a free alternative to popular spreadsheets like Microsoft Excel. I’ve tried OpenOffice previously, and it’s a really capable option. You can also use the free personal finance templates supplied by Google Docs or Savvy Spreadsheet.

- Once you’ve disciplined yourself to spend less than you make, tracking spending can help you optimize your finances and get the most out of your money.

- And last but not least, remember that the tool you use is not the most important factor. What matters is your willingness to actively manage your finances.